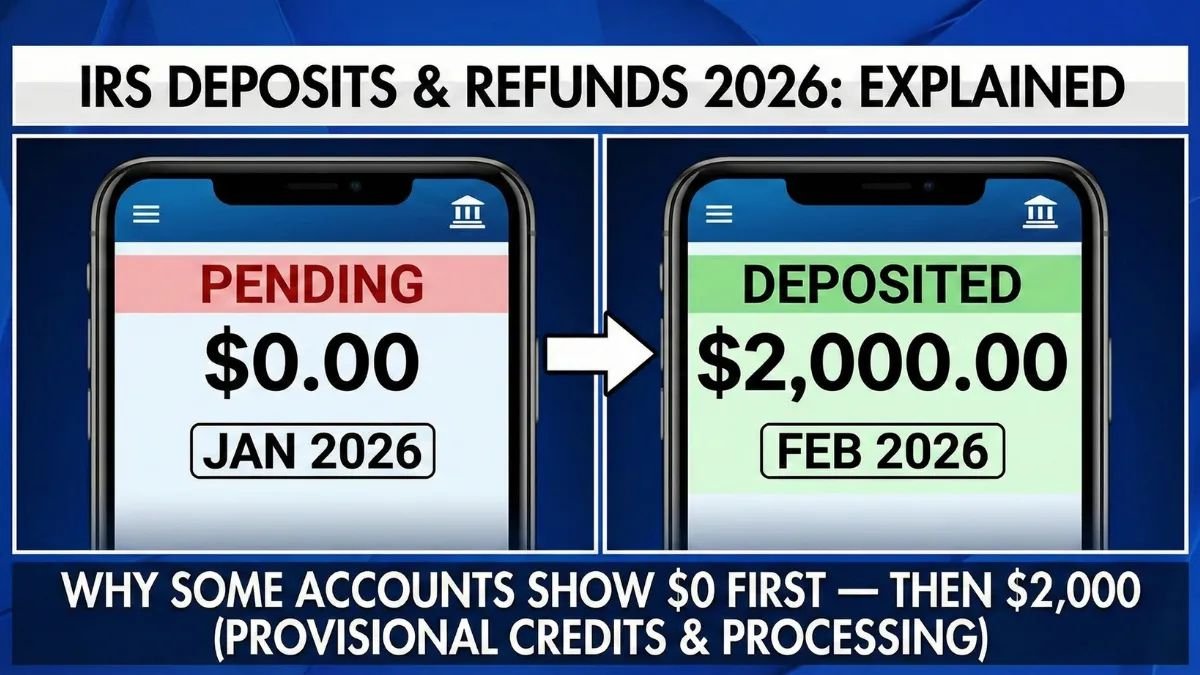

Have you checked your bank account in early 2026 and spotted a strange $0 IRS deposit that suddenly turns into $2,000? This common occurrence leaves many taxpayers confused and concerned, often mistaking it for a rejected refund or glitch. In truth, it’s a normal part of how banks handle IRS direct deposits, designed to verify transactions securely before releasing your full tax refund 2026.

By understanding this behind-the-scenes process, you can avoid unnecessary stress and skip hasty decisions like filing amendments. This guide breaks down the mechanics, timelines, and steps to monitor your refund confidently, ensuring you get every dollar owed without delays.

Decoding the $0 Placeholder in IRS Deposits

The $0 entry, often labeled as “TREAS 310” or similar, appears when your bank receives initial notification of an incoming IRS payment via the Automated Clearing House (ACH) network. This temporary hold acts as a security measure, confirming the transfer’s legitimacy before posting the actual amount.

Think of it like a pre-authorization on your debit card during a purchase—it’s not a deduction but a flag for pending funds. This step protects against errors or fraud, especially for government payments.

- Prevalent in IRS refunds, stimulus checks, and federal benefits.

- Typically updates within 1-3 business days after IRS release.

- Holidays or weekends may add a day or two due to processing batches.

Seeing this isn’t a warning sign; it’s confirmation your tax refund 2026 is on its way. Pair it with official IRS tracking for peace of mind.

Common Triggers for the Placeholder

Banks use placeholders to match incoming data with your account details, including routing and account numbers. Mismatches here can prolong the hold, but they’re rare with accurate e-filing.

Fraud detection algorithms also play a role, scanning for unusual patterns before finalizing credits. Once cleared, the $0 vanishes, revealing your full refund.

IRS Refund Processing Timeline for 2026 Filers

Once your e-filed return is accepted, the IRS targets issuing direct deposit refunds within 21 days, though audits or ID verifications can push this out. Funds then enter the ACH system, where banks receive them in bulk for review.

Paper checks take far longer—up to six weeks or more—making electronic transfers the go-to for speed in 2026. Issues like mismatched SSNs or unreported income trigger IRS notices, pausing everything until fixed.

- Track progress daily with the IRS2Go app or “Where’s My Refund?” tool on IRS.gov.

- “Pending” status indicates funds en route, not problems.

- Most deposits land smoothly; patience is key during peak filing season.

Your bank’s policies determine final posting. Some credit instantly upon ACH receipt; others wait for full settlement to comply with federal regulations.

Factors Influencing Deposit Speed

High-volume periods like January and February slow things due to millions of returns. Credits involving dependents or income verification add extra layers of review.

Opt for banks with early direct deposit perks to shave off 1-2 days, giving you quicker access to your money.

Why $2,000 Refunds Frequently Show $0 First

Refunds around $2,000 often combine federal withholdings with refundable tax credits like the Earned Income Tax Credit (EITC), Additional Child Tax Credit (ACTC), or American Opportunity Tax Credit (AOTC). These require thorough IRS eligibility checks, increasing scrutiny.

EITC and ACTC payments, for instance, may hold until mid-February for fraud prevention. Banks, noticing sums larger than your usual activity, trigger automated scans that display the $0 temporarily.

Interest on overpayments, calculated as additional income, can tweak the final amount, prompting further validation. This routine process ensures accuracy but makes mid-range refunds like $2,000 seem delayed.

- Credits drive 70% of refunds over $1,500, per IRS data patterns.

- Fraud flags are higher for these blended payments.

- Verifications resolve automatically in most cases.

Avoiding Common Missteps with These Refunds

Don’t assume rejection based on the placeholder—it’s standard for credit-heavy returns. Rushing to amend can backfire, extending your wait by months.

Instead, document everything and use official tools to verify status before acting.

IRS Approval vs. Bank Posting: What You Need to Know

When the IRS marks your refund as “issued,” it’s sent—but your bank controls when it appears in your balance, guided by funds availability policies. Federal rules allow next-day access for government deposits, yet internal holds persist.

Bank variations explain why one person sees instant credits while another waits days. Check your account agreement or contact support for their specific timelines.

Proactive filers using direct deposit early in the season benefit from lighter queues, minimizing placeholders.

Red Flags and When to Act

A $0 lasting over five business days merits a bank inquiry, not an IRS call. Negative balances or error codes are true concerns; otherwise, it’s business as usual.

- Stick to IRS.gov over social media for accurate info.

- Tax professionals help with complex issues like offsets.

- Amended filings should wait for confirmed problems.

Step-by-Step Guide to Tracking Your 2026 Refund

Start with IRS tools for issuance status, then monitor your bank app for placeholders. Set alerts for transactions labeled “IRS” or “Treasury.”

If no update after issuance, contact your bank first—they handle pending details best. Prepare with SSN, filing date, and expected amount for IRS hotline if needed.

- Request a payment trace only after 21 days post-issuance (takes weeks).

- Keep records of all communications.

- Peak times mean longer holds; plan accordingly.

For persistent issues, consult a tax advisor to navigate offsets or errors efficiently.

Key Takeaways for Stress-Free Tax Refunds

The shift from $0 to $2,000 is a reliable sign of progress in IRS deposit 2026 handling. Banks and the IRS collaborate seamlessly, with placeholders bridging the gap.

Arm yourself with knowledge: use verified tools, understand timelines, and resist knee-jerk reactions. Your refund will arrive as promised, turning anticipation into satisfaction.

In conclusion, embrace the process—regular checks via IRS resources ensure you stay ahead. With direct deposit’s efficiency, 2026 filers can focus on financial wins rather than worries, securing every cent of their hard-earned refund.